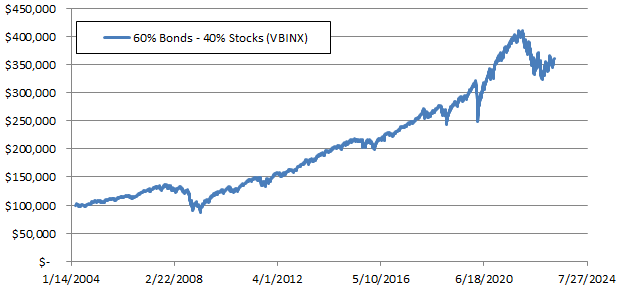

Treasury Bonds & Short VolatilityWhen we think about retirement and growing our retirement saving account, what we want is an investment vehicle that delivers steady returns with a drawdown as small as possible. Traditionally we are advised to invest in a combination of stocks and bonds. As these two assets classes are inversely correlated, it is common belief that they offer downside protection during rainy days for the equity market. Is it really the case? The Vanguard Balanced Index Fund, ticker VBINX, that invests 60% in bonds and 40% in equities says otherwise. The chart below shows that such portfolio can experience large drawdowns relative to the annualized return. This is something that we do not really want. First because it is emotionally intensive to handle 35% maximum drawdown (it is not unlikely the portfolio holder might sell low). Second because it will take several years to recover from the drawdown. Let’s not get fooled by the idea of equities diversification. When the equity market goes south, equities and different asset classes become all closely correlated thus offering very little downside protection; read more in here.

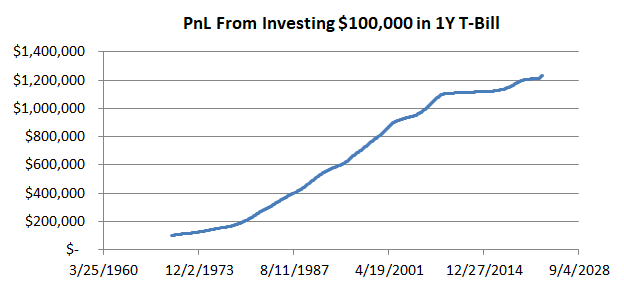

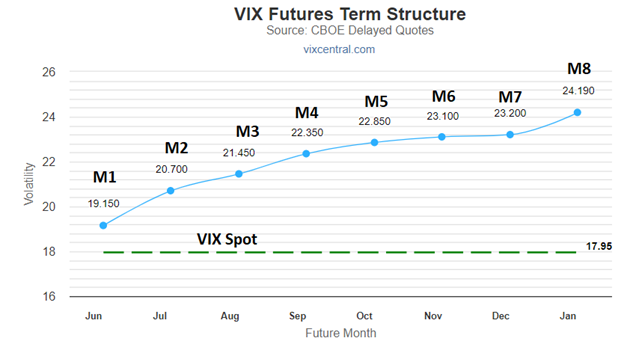

We can think of going one step ahead and using the Efficient Frontier Portfolio to best identify what equities and bond ETFs to include in our account. In this case we get into a trade-off between relative portfolio volatility (Sharpe ratio) and annualized returns (CAGR). More on how the numbers in the table below were generated in here.  Is there a way out? Can we get steady returns and decent CAGR without day trading? In my opinion yes but we need to rethink the instruments we use. Short dated high quality bonds, should be still a part of the portfolio. If held to maturity, 1 year lock up period is acceptable, can deliver a steady return with virtually no drawdowns; assuming there is no default on payments. Let’s keep in mind that we might have a recency bias. In the last 10-15 years the Treasury Bond yields have been nearly 0% thus many investors have consider them unattractive. If we look at the yields on a larger time horizon, this is not the case. Considering the inflation we are experiencing, the ending of the era of easy money,… it will not be unlikely that in the long run T-bond yields will land in the 3 to 5% territory (1 to 2 percentage points above the inflation rate) thus potentially becoming appealing again to many retirement accounts.  We now need a second component to boost the CAGR without compromising much the volatility and drawdown of the portfolio. Historically this second component has been equities. Equities have large drawdowns relative to their CAGR and if we assume that in the next decade the equity market will not trend upwards as during the 2010s because of a stickier inflation and tighter economic policies, we then need to look elsewhere. In my opinion short volatility products should become the second part of the portfolio. ETPs like SVXY and SVIX derive their value from the front two months VIX futures term structure. The front two months, M1 & M2, naturally decay toward the VIX spot value. This decay and the absolute price movement of the futures are the drivers behind the price variation of SVXY and SVIX. With the few exception of the VIX futures spiking as result of elevated equity market fear, the vast majority of time, they decay towards the VIX spot value.  Blindly using this products is not advisable. When M1 and M2 are slightly above or below the VIX spot price, these products nose dive. If we have a very simple rule and we say that we do not use these products when the two VIX futures front months are below the VIX spot value increased by 2.5% then we are better off; see chart. Is it day trading? Not really because we are talking of 2 to 3 trades per month.

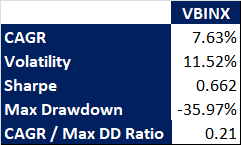

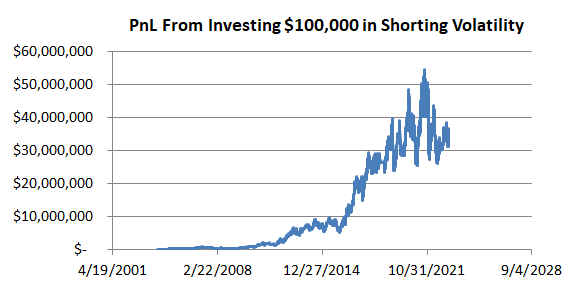

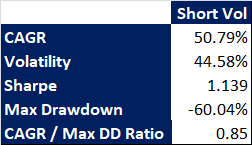

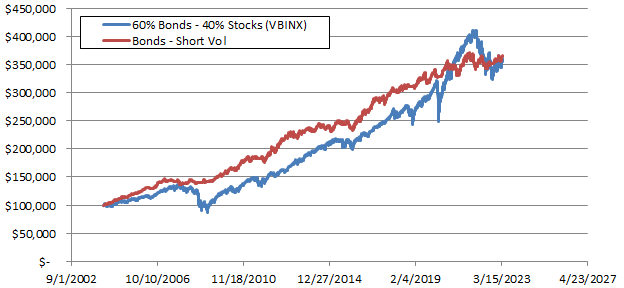

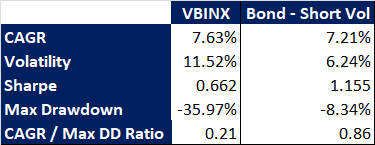

The PnL from shorting volatility might look very volatile at first with a high drawdown, but at a second look it is not. Let me explain, if a short vol product experiences a drawdown of 60%, it will take a bit more than 1 year to break even given that the annualized return is ca. 51%. In the case of the traditional 60-40 portfolio, after experiencing a drawdown of 36%, it will take 4.7 years given that the CAGR is 7.63%. Do you still think it is volatile? Let’s now put short term dated bonds and shorting volatility together. For the sake of comparing to VBINX, I have chosen to allocate 14% to the short vol position so that the CAGR of the two approaches is comparable. Despite, I believe that 7.5 to 10% is a more appropriate allocation because of the better CAGR to maximum Drawdown ratio. For the same CAGR as VBINX, the current approach reduces the drawdown by 4.5 times while nearly doubling the Sharpe ratio.

There is a value to consider an alternative to equities to the traditional 60-40 balanced portfolio. According to the way I see it and what the numbers say, this alternative is called shorting volatility. Better drawdown and more consistent returns

|

|

|

Questions?Contact us here.

DisclaimerThe information, analysis, data and articles provided in this and through this website are for informational purpose only. Nothing should be considered as an investment advice. Alpha Growth Capital does not make any recommendation to buy, sell or hold any security or position. The website and information provided through it are marketed “as is”. There is no guarantee that anything presented and provided on this and through this website is complete, accurate and correct. Relying on the information provided on this website and through its communication channels is done entirely at the individual own risk. There is no registration as investment advisor under any security law and nothing provided in this and through this website should be interpreted as a solicitation to buy, hold or sell any mentioned financial product or service. Past performance is not indicative of future results. Any financial decision is at the sole responsibility of the individual.

By navigating in this website, you agree to its Terms & Conditions |