|

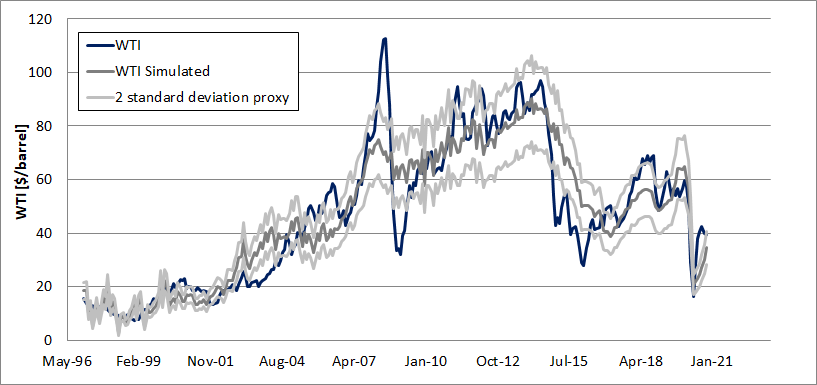

Successful investors and traders use a variety of investing techniques. Some are more profitable than others but the line in between succeeding and failing is the decision making process. All the successful traders and investors have one thing in common: they know when to enter and exit each single trade. One of the investing techniques that several people are using is price arbitrage. With this approach, the investor estimates the fair price of equities, commodities or you name it and if there is a large enough gap between the fair estimated value and the spot price then a position is entered. Position are opened either long or short depending whether the fair value is above or below the spot price. In the past I have built a couple of these models: the first to estimate the value of the S&P500 while the second the fair price of gold (here). In this article, I’ll present the work that was done in modeling the oil price of the West Texas Intermediate; WTI in short. Crude oil is a commodity and as such it follows the law of supply, demand and inventories. At constant demand, increasing the supply, the inventories go up and the price goes down. With lower supply the opposite happens. When the supply is constant and the demand decreases (what happened in early 2020 due to the COVID-19), the inventories tend to build up and the price goes down. With higher demand, the opposite happens. The WTI model that was built was based solely on the law of supply and demand. The simulated WTI price follows quite well the actual price with an accuracy of 82% and a proxy of two standard deviations of 18%. Sudden market movements due to excessive market buying or selling sentiment are not well captured; e.g. 2007-2009 and 2014-2015.  The next question that might come to mind is: how do I use it?

Let me start with how I do not use it. When I see a large enough gap between the fair and spot price, I never buy or short sell any future contract or ETPs. This is because I do not know when the two prices will converge and whether the market is gona rally in the opposite direction of the fair price. Few macro firms went bankrupt while following this approach. The way I use the model is to guide my decisions when deciding what option strategy to use. With small to non-existent price gap I tend to use neutral strategies. When the fair price is above the spot, I go with a bullish strategy while bearish in the opposite case. It goes without saying that the choice of the strategy should be made together with the current volatility rank of the WTI while properly selecting the position size and keep enough money in the account in the eventuality the option contract is assigned. If you have enjoyed the article, leave your comment below. If you find the model useful and you would like to use it, then click the link. |

|

|

Questions?Contact us here.

DisclaimerThe information, analysis, data and articles provided in this and through this website are for informational purpose only. Nothing should be considered as an investment advice. Alpha Growth Capital does not make any recommendation to buy, sell or hold any security or position. The website and information provided through it are marketed “as is”. There is no guarantee that anything presented and provided on this and through this website is complete, accurate and correct. Relying on the information provided on this website and through its communication channels is done entirely at the individual own risk. There is no registration as investment advisor under any security law and nothing provided in this and through this website should be interpreted as a solicitation to buy, hold or sell any mentioned financial product or service. Past performance is not indicative of future results. Any financial decision is at the sole responsibility of the individual.

By navigating in this website, you agree to its Terms & Conditions |